The Shortage That Isn't

The country does not lack pediatricians. It lacks pediatricians in the places and on the payers that the economics cannot support — and calling that a workforce shortage points the remedy in exactly the wrong direction.

I. The word that ends the inquiry

There is a particular comfort in the word shortage. It names a problem and prescribes its own remedy in the same breath: if there are too few of something, make more of it. Train more, fund more residency lines, recruit earlier, expand the pipeline. The word does the analytic work before the analysis begins, and the conversation that follows is about throughput rather than structure.

For the better part of a decade, “pediatric workforce shortage” has been the standing frame for why families in large parts of the country cannot find a pediatrician — and certainly cannot find a pediatric subspecialist — within any reasonable distance of where they live. The frame is repeated in association statements, in grant rationales, in the preambles to legislation, in the trade press. It has the great advantage of being half true, which is what makes it durable. There are real and painful gaps in access. Children do wait months for a developmental-behavioral evaluation; rural counties do go without a single pediatric presence.

But the inference from those gaps to a headcount shortage is the place the reasoning quietly breaks. A gap in access is evidence that pediatricians are not where the need is. It is not, by itself, evidence that there are too few of them. Those are different diagnoses, and they call for opposite remedies. One says make more. The other says the ones you have are being pushed somewhere else, and you should ask what is doing the pushing.

This article argues for the second diagnosis. The pediatric problem in the United States is overwhelmingly a problem of distribution and compensation, not of supply. There are enough pediatricians. The economics route them away from the geographies and the payers that need them most, and the shortage frame obscures the routing by treating the symptom — empty exam rooms in the wrong places — as if it were a quantity.

II. The aggregate that doesn’t behave like a shortage

Start with the number the frame relies on you not to examine: how many pediatricians there actually are, and which way the line is moving.

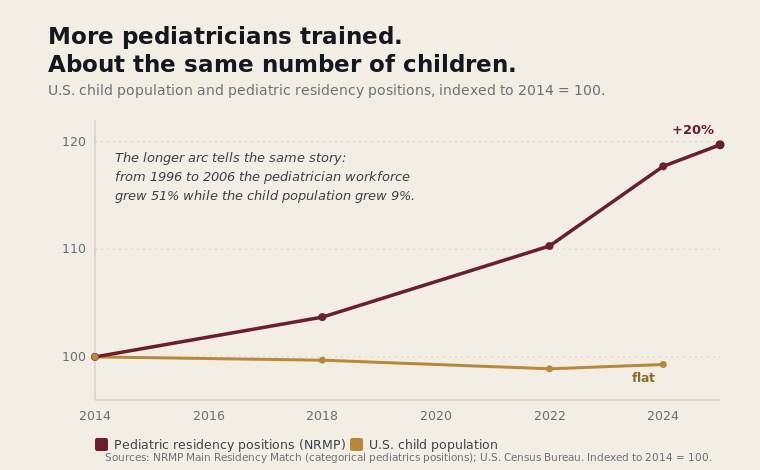

A genuine workforce shortage has a signature. The supply curve flattens or falls; entry into the field declines; the people in it are aging out faster than they are replaced. Pediatrics does not show that signature. By the standard counts, the supply of pediatricians has risen for decades, and faster than the population it serves: between 1996 and 2006 the general-pediatrician workforce grew by 51 percent while the child population grew by 9, and across the longer arc the number of pediatricians per 100,000 children more than doubled. The doctors were produced. The children did not multiply to match.

The training pipeline tells the same story from the other end, though it has wobbled lately in a way worth being honest about. In the 2024 Match, categorical pediatrics filled 91.8 percent of its positions — a real drop from 97.1 percent the year before that drew genuine alarm — before rebounding to 95.3 percent in 2025. Set the alarm in proportion: a specialty that fills better than nine of every ten training slots in its worst recent year is not one the country has stopped producing. And the dip itself, as a later section will argue, looks less like waning interest in children than like medical students reading the same price signal everyone else in this article is reading.

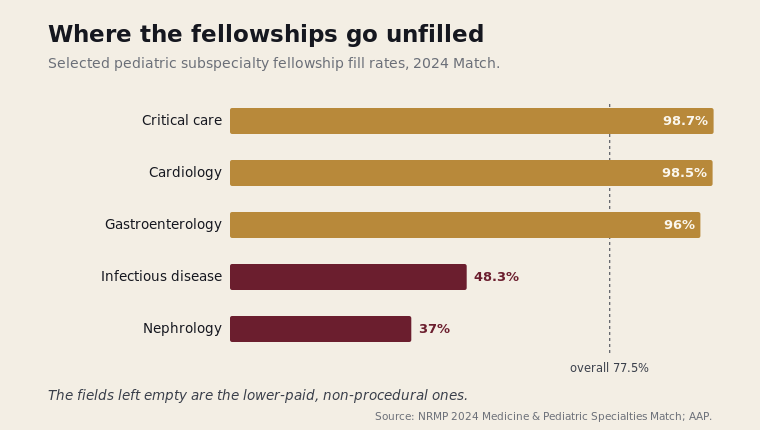

What is true — and what the aggregate hides — is that the subspecialty pipeline behaves very differently from the general one, and that the difference is itself economic rather than demographic. Several pediatric subspecialties leave fellowship positions unfilled year after year, and the unfilled ones cluster with striking regularity in the lower-compensated, non-procedural fields. In the 2024 subspecialty match, pediatric nephrology filled just 37 percent of its positions and infectious diseases 48 percent, even as the procedural, better-paid subspecialties filled comfortably; the AAP’s own reading is that compensation, weighed against a trainee’s debt, is doing the choosing. That is not a population running out of doctors. That is a population of doctors responding to a price signal.

The fill rate, though, is only one face of the number, and honesty requires the other. The subspecialty pipeline has not shrunk — it has grown. The count of pediatric subspecialty fellowship positions has risen in absolute terms since 2008, across nearly every field, and the number of first-year fellows has climbed with it; the training enterprise is producing more pediatric subspecialists, not fewer. Both things are true at once — more subspecialists trained, and families in much of the country still unable to find one — and why the rising numbers have not become rising access is a question this article leaves with the reader. But the two facts belong side by side, because a story told with the fill rate alone is missing half its evidence.

A field cannot be genuinely short of bodies and fill almost all its training positions at the same time. The signature of a real shortage is missing.

If the aggregate supply is adequate and the front door is crowded, then the access gaps families experience are not being produced by scarcity. They are being produced by something downstream of supply — something that decides where an adequate number of pediatricians end up practicing, and which children they end up seeing.

III. The two forces that do the routing

Two forces do most of the routing, and they are not mysterious. They are visible in any practice’s accounts receivable.

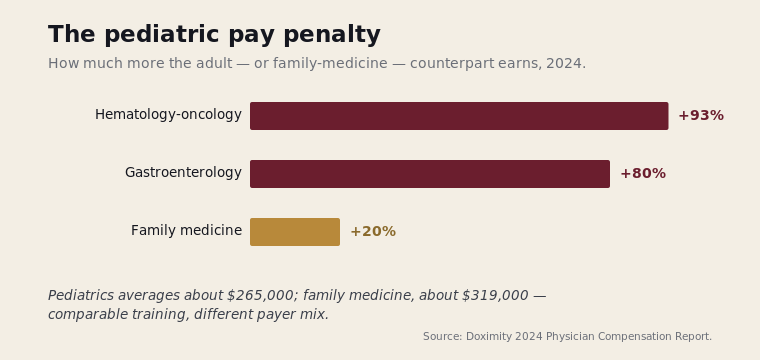

The first is the payer. Pediatrics is the most public-payer-dependent of the major fields, and not by a little: 49 percent of American children — some 37 million — are covered by Medicaid or CHIP, a reliance no adult primary-care specialty approaches, and one that ranges by state from 18 percent of children in Utah to 71 percent in New Mexico. In many pediatric practices Medicaid is the majority of the panel. Medicaid reimburses physician services well below Medicare — about 71 percent on average, and 69 percent for the office visits that are the substance of pediatric work — and Medicare in turn pays below commercial rates. The arithmetic stacks against the specialty whose patients are concentrated in the lowest-paying payer: pediatricians sit at or near the bottom of every compensation ranking, earning roughly $265,000 to a family physician’s $319,000 for comparable primary-care work, with the adult-versus-pediatric gap reaching 80 percent in gastroenterology and more than 90 percent in hematology-oncology.

This is not a story about greed. It is a story about arithmetic that any practice owner is forced to do. A practice cannot operate at a structural loss on the bulk of its panel and remain open. So the panel composition that the need requires — heavily Medicaid, heavily young — is precisely the panel composition the reimbursement system makes hardest to sustain. The children who most need a pediatrician are, in payer terms, the children a practice can least afford to fill its schedule with.

The second force is geography, and it is largely the first force wearing a map. Rural and lower-income communities have higher Medicaid penetration, thinner commercial coverage, lower patient volumes, and longer distances between paying visits. A pediatrician who opens in such a community is choosing to be paid less, by lower-paying payers, with less of the commercial cross-subsidy that keeps an urban or suburban practice solvent. The distribution that results is staggeringly uneven: a landmark analysis in Pediatrics found per-capita pediatrician supply varying more than sixfold across local markets, with roughly a million children living in areas with no local child physician at all — even as the national supply climbed. The market, behaving exactly as a market does, sends physicians toward higher-paying payers and denser commercial coverage — which is to say, toward the places that already have pediatricians and away from the places that do not.

Stack the two forces and the access map predicts itself. The shortage is not where the pediatricians are absent in number. It is where the economics will not let them stay.

IV. Who you end up working for

The economics do not stop at deciding where a pediatrician practices. They increasingly decide whether a pediatrician practices for herself at all — and that decision is the same arithmetic, run one level up.

Independent practice has been contracting across American medicine, and pediatrics has not been spared. By the American Medical Association’s Physician Practice Benchmark Survey, the share of physicians in physician-owned private practice across all of medicine fell to 42.2 percent in 2024, from 60.1 percent in 2012; for the primary-care specialties — pediatrics, internal medicine, family medicine — the figure sits lower still, in the high-thirties to low-forties. (An office that still looks independent from the waiting room is, increasingly, owned by a hospital or a large group.) The other side of that ledger is employment: the same survey put 34.5 percent of physicians in hospital-owned practices and another one in eight employed directly by a hospital in 2024, and the Physicians Advocacy Institute’s 2024 study with Avalere, which counts every corporate employer, put the employed share at 77.6 percent. When the AMA asked physicians who had sold their practices why, the most common answer was not lifestyle or retirement. It was payment: 70.8 percent named the need to negotiate better rates with insurers as an important reason for the sale.

That answer is the thread back to the rest of this article. A pediatric practice carrying a heavily Medicaid panel cannot manufacture the one thing that keeps an independent practice solvent — leverage with commercial payers. A large employed group or health system negotiates commercial rates from a position of scale a solo or small pediatric practice cannot approach; selling into one is, among other things, how a physician buys access to those rates. The independent practice depends on a payer mix that the Medicaid-heavy pediatric panel is precisely the wrong shape for. So the same arithmetic that routes pediatricians away from Medicaid-dense geographies also routes them out of ownership and into employment.

And because that arithmetic begins with the Medicaid fee schedule, the pressure is not uniform across the country — it is as uneven as Medicaid itself. Medicaid pays physicians, on average, about 71 percent of what Medicare pays, and only 69 percent for the office visits that are the substance of pediatric practice. But the national figure hides an enormous spread: the same Urban Institute analysis finds the state fee index running from roughly 37 percent in Rhode Island to above the Medicare rate itself in a handful of rural states — a state paying its physicians barely a third of what Medicare pays sits in the same country as one paying more than Medicare does. Where the index sits lowest, independent pediatric practice is hardest to sustain.

It is a reasonable inference — though not, to my knowledge, a finding any single study has yet established for pediatrics specifically — that the pull out of ownership is strongest in exactly those lowest-index states. The supporting evidence comes from adjacent settings: when private-equity and corporate buyers acquire practices and hospitals, they shift their patient mix away from Medicaid and toward commercial payers, most sharply in states with the widest Medicaid-to-commercial payment gap. The buyers are chasing the same commercial revenue the independent practice needs and cannot get — which produces the hardest version of the mechanism. The practices most squeezed by low Medicaid rates, small and Medicaid-dense and in low-income communities, are also the least attractive targets for the consolidation that absorbs everyone else. In the lowest-reimbursement places a struggling pediatric practice may find no buyer at all: it does not consolidate, it closes, or it never opens. The result is a community with neither an independent pediatrician nor an employed one — the empty exam room the shortage frame points to, produced not by a national lack of doctors but by a local fee schedule that could sustain neither kind of practice.

V. What the trade costs

The shift is not simply a loss, and it should not be told as one. Employment has given many pediatricians what independent practice could not reliably offer: a salary insulated from a Medicaid-heavy payer mix, relief from billing and overhead and the operational weight of running a small business, and the negotiating scale a system brings. What it has cost is autonomy — and the cost is visible in the data. Physician burnout reached near-record levels in 2024, around six in ten physicians, and the loss of day-to-day clinical control that comes with consolidation tracks closely with the dissatisfaction beneath it. The trade on offer is income stability for clinical autonomy, and the burnout figures suggest the second half of the bargain is heavier than it looked.

The family’s side of the ledger is harder still. As independent pediatric practices thin out and care concentrates in hospital-owned systems, families’ choices narrow with them — most sharply for those with the least bargaining power. Narrow-network plans are common on the ACA marketplace, and individual and small-group plans have steadily cut their out-of-network coverage; a family buying its own insurance, or covered through a small employer, increasingly finds that the only in-network pediatric care is whatever the dominant local system runs.

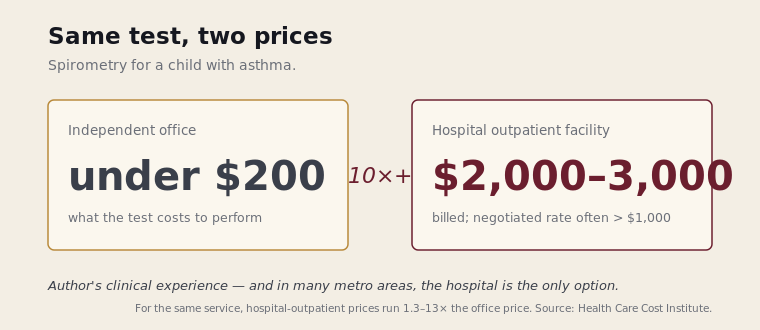

And the same care costs more inside that system. A service delivered in a hospital outpatient department is reliably priced above the identical service in an independent office — by a documented 1.3 to as much as 13 times, with hospital-owned offices charging about 26 percent more on average, largely because of an added facility fee. The squeeze is tightest in the subspecialties, where independent practice has all but disappeared: in one survey of the pediatric pulmonary workforce, 96 percent practiced in academic institutions and just 2 percent in private practice. The abstraction turns concrete in my own field. A spirometry test — the breathing measurement a child with asthma may need several times a year — runs under $200 in an independent office. In the hospital-based facilities that, across many metropolitan areas, are now the only place a child can get one, I have seen the same test billed at $2,000 to $3,000, with the insurer’s negotiated rate — pegged to a percentage of that sticker — still landing north of $1,000.

Who absorbs that difference depends on the plan, and a growing share of families are on the plans that absorb all of it. Roughly a third of workers with employer coverage now hold high-deductible plans, and on one of those the family pays the full negotiated price until the deductible is met. A child with well-controlled asthma, seen in an independent pulmonary office, might never have spent enough to reach the deductible at all. The same child, routed to a hospital facility because no office-based pediatric pulmonologist exists within reach, can exhaust the deductible and march toward the out-of-pocket maximum on breathing tests alone. The shortage frame would call that a child who finally got access. The family would call it a bill.

VI. The test the frame cannot survive

There is a clean way to tell a distribution problem from a supply problem, and it costs nothing to run.

Ask what would happen if you produced more pediatricians without changing anything else — without touching the Medicaid fee schedule, without altering the rural payer mix, without changing what a subspecialty fellowship pays relative to a procedural one. Under a true supply shortage, the new graduates would flow toward the unmet need, because unmet need would mean unfilled, payable demand. Under a distribution-and-compensation problem, the new graduates would face the same price signals their predecessors faced, and would sort themselves the same way: toward the better-paying payers, the denser commercial markets, the higher-compensated subspecialties. The underserved county and the under-filled fellowship would remain underserved and under-filled. You would simply have added pediatricians to the places that already had them.

That second outcome is, broadly, what decades of pipeline expansion have already produced. The general-pediatrician workforce grew by half in the decade to 2006 while the child population barely moved, and yet the rural counties and the underserved markets gained little or nothing; the additional doctors settled where doctors already were. A remedy aimed at quantity has not closed a gap that was never primarily about quantity. That is not a failure of effort. It is a sign that the diagnosis was wrong.

The frame cannot survive this test, because the frame’s entire remedy is make more, and make more is precisely the intervention the test predicts will not work. A frame whose prescription has already been tried, and has already failed to move the thing it was meant to move, has earned a harder look at its premise.

VII. What is at stake in the word

It would be easy to treat this as a quarrel over terminology, the kind of thing that does not matter outside a faculty meeting. It is not. The word governs where the money goes.

If the problem is a shortage, the rational public investment is in production — residency slots, loan-repayment-for-pipeline, recruitment campaigns. If the problem is distribution and compensation, that investment is largely wasted motion, and the rational interventions are different in kind: raising the floor on what the lowest-paying payer pays for pediatric work, so the panels the need requires are not the panels that break a practice; building compensation structures that do not penalize the cognitively intensive, lower-procedural subspecialties relative to the procedural ones; making the underserved geography solvent rather than merely staffing it once and watching it empty again.

The shortage frame is comfortable for a reason worth naming plainly. Make more asks nothing of the payers. It does not touch the fee schedule, does not implicate the commercial-Medicaid spread, does not ask why the specialty that sees the most children is paid the least to do it. It locates the problem in a quantity that more spending on training can fix, and locates it nowhere near the parties who set the prices. A diagnosis that exonerates the payment system is always going to be the more popular diagnosis. That popularity is not evidence that it is correct.

The honest version is less comfortable and more useful. The country has enough pediatricians. It has built a payment and distribution system that cannot keep them where the children are, and then named the empty exam room a shortage so that the remedy could be something other than fixing the system that emptied it.

The next time the phrase pediatric workforce shortage arrives — in a press release, a grant, a bill — there is a question available that the phrase is built to forestall:

If we made a thousand more pediatricians tomorrow, where would they go — and would it be where the children are?

The answer is in the fee schedule, not the pipeline.

Satyanarayan Hegde, MD, is a pediatric pulmonologist and the founder of Access Pediatric.